How much do we actually need for retirement?

Accoording to the recent Retirement Spending report published in September 2022 New Zealanders have a new factor to consider in their retirement planning: inflation. Although we have experienced higher rates in the past, that was more than 30 years ago, and is therefore a distant memory for most. Retirement represents a substantial life change for most New Zealanders. It is often included in lists of the most stressful life events. Without good preparation and planning, many New Zealanders will find it challenging to achieve the expectations and aspirations they hold for their future retirement.

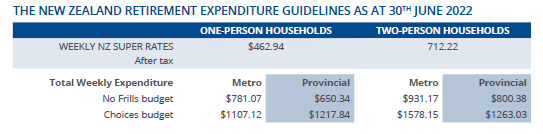

The Retirement Expenditure Guidelines provide information about actual levels of expenditure by New Zealanders who have already retired. Expenditure patterns change over time due to societal changes and the effect of inflation. This report addresses these changes with an adjustment for inflation to 30th June 2022. The No Frills guidelines reflect a basic standard of living that includes few, if any, luxuries. The Choices guidelines represent a more comfortable standard of living, which includes some luxuries or treats.

KEY FINDINGS IN THIS REPORT

• Most New Zealanders aspire to a better standard of living in retirement than can be supported by NZ Superannuation alone.

• Most households where NZ Superannuation is currently a source of income have achieved this.

For 2 person households in the provincial areas, their choices retirement spend has come in at $65,677 per annum and the for single households this was $63,327.

NZ Superannuation is CPI/ Inflation adjusted every year. Below includes the previous increase amounts of NZ superannuation.

While we should anticipate that the Reserve Bank of NZ (RBNZ) will once again get inflation back to its target range (1-3%), it may take time to achieve that. In the meantime, there are ways to manage for inflation. These include reviewing your expenditure and making mindful spending choices in order to avoid the need to draw down larger amounts than planned, which is not necessarily as easy as it sounds. It’s also important to think about where your funds are invested, whilst it is very tempting currently to move everything to cash for reduced volatility this may not be the best option to support income streams over the long retirement period ahead.

For a full copy of the report please email lisa.bentley@peak.net.nz

Many thanks,

Lisa Bentley

Financial Adviser FSP:768453

Peak Portfolio Management

Mobile: 029 200 4090

Address: 200 Market St North, Hastings, 4122